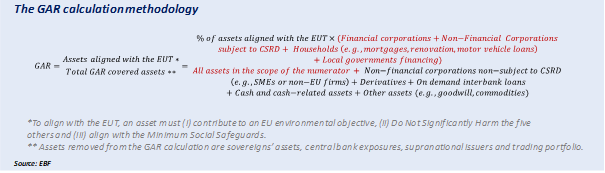

In 2024, Financial Institutions (FIs) are unveiling their Green Asset Ratio (GAR) for the first time. During the previous years, FIs were only disclosing the ’eligibility version’ of this indicator1. GAR’s publication constitutes an important step to help stakeholders understand how, and to what extent, FIs’ assets align with the European Union Taxonomy (EUT) environmental objectives – an essential tool in the EU Sustainable Finance Framework2. Indeed, the indicator is a ratio between the EUT aligned assets and the total GAR covered assets (assets included in the denominator). However, given the numerous criticisms voiced by the banking industry regarding this indicator, this inaugural publication might be perceived as a crash test that could potentially affect its future credibility.

2023 Integrated Annual Reports (published in 2024) have validated the forecasts made by the European Banking Agency (EBA) in its EU-wide pilot exercise on climate risks conducted in 20213 - GAR levels (turnover KPI4) would be exceedingly low. Indeed, while the average % of eligible assets reaches 36.5%, the average GAR (% of aligned assets) calculated by our team only stands at 2.5% (based on a sample of 24 FIs).

To manage stakeholders’ expectations, FIs have been actively communicating GAR’s limitations through various channels such as the European Banking Federation (EBF)5, their Integrated Annual Reports, etc. They have been specifically highlighting that the indicator is structurally low and misleading and that comparability is challenging as the indicator is heavily influenced by each FI’s business model (e.g., exposure to companies non-subject to Corporate Sustainability Reporting Directive (CSRD)). Additionally, accessing data supporting asset EUT alignment, especially in the retail segment, presents a real challenge.

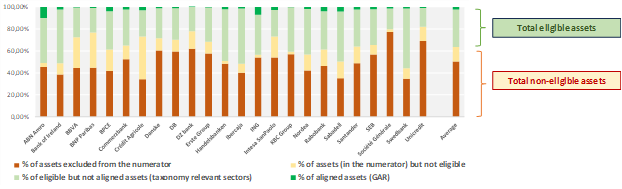

Graph 1: Breakdown of total GAR assets (denominator) for a sample of 24 European banks (in %)

Source: 2023 Integrated Annual Reports (published in 2024)

Graph 1 shows several statistics illustrating FIs comments as, in average, 50.1% of the assets included in the denominator are excluded from the numerator significantly capping the GAR level, and 13.4% included in the numerator are not eligible to the EUT. We also note that, in average, 31.6% of the total assets are excluded from the GAR denominator6.

There is limited visibility on how the Commission will review and integrate FIs ’feedback and update GAR’s methodology. Also, according to an article published by Environmental Finance, such review is not likely to happen before 2025. However, in its guidance on ESG risks disclosures, the EBA has been already proposing a complementary (but comparable) indicator to address some of the GAR’s limitations: the ’Banking Book Taxonomy Alignment Ratio’ (BTAR)7 that should be disclosed by FIs soon.

We appreciate the comprehensive comments made by FIs regarding the need for stakeholders to be careful when interpreting the GAR. We also concur that there is substantial room for improvement in its design. However, we also recognize the enhanced transparency facilitated by the indicator and are of the opinion that the crash test is not really a complete failure.

First, the detailed elements provided by FIs on GAR’s calculation already help to overcome certain limitations. Despite the indicator structural constraints, readers have direct insights into eligible assets and aligned assets, thereby providing clarity on the portion of eligible assets aligning with the EU taxonomy (averaging at 6.5% based on our sample). While this quick recalculation is far from solving all limitations, it addresses partially the lack of consistency between the numerator and the denominator, and the comparability challenge. It also enables to draw the following conclusion – alignment levels remain low and, beyond GAR’s design limitations, FIs still need to actively work on their contribution to the EU environmental objectives.

Then, the granularity proposed by the GAR disclosure template facilitates the identification of low-hanging fruits and potential engagement topics with FIs for sustainable investors. One significant opportunity lies in implementing measures to actively address the ’mortgage’ portfolio, as it constitutes most assets eligible under the EUT but still has a very limited alignment with it. Indeed, while loans granted to households (mostly composed of mortgages8) represent, in average, 88.8% of the EUT eligible assets, a very limited portion of those eligible assets are aligned with the EUT (usually less than 5%). Interestingly, the assets deemed ‘most eligible’ (in terms of volume), are also the most impacted by the EUT usability challenge, primarily due to data scarcity in the retail segment (even if FIs are not required to meet minimum social safeguards for mortgages ), but also due to the still relatively low energy efficiency in European buildings (compared to stringent EUT criteria). Some FIs even indicate that not a single mortgage in their portfolio aligns with the EUT. Others express a slightly more optimistic outlook, reporting a relatively high level of alignment (with alignment figures around 20%), often coupled with the highest GAR levels. FIs with higher GARs attribute this to the relatively higher energy efficiency of buildings in their jurisdictions (supporting the contribution to the Climate Change Mitigation EUT objective). They also provide insights into the processes employed to conduct internal physical risks assessments (supporting the alignment with the Climate Change Adaptation Do Not Significantly Harm criteria9). However, readers should exercise caution as higher alignment figures may not necessarily reflect better practices but could simply result from ‘’different interpretations on how certain Taxonomy criteria must apply’’, as noted by the EBF.

This might be another important lesson learned during this crash test - the GAR calculation has prompted FIs to realize how important the EUT usability challenge was. There is now a need for stakeholders to identify, evaluate and propose different approaches to foster the emergence of best practices on how to support and disclose alignment, and how to support their clients (mainly corporates and individuals) to get closer to the EUT standard. Initiatives have already started, with the EBA proposing, for example, a ‘’simplified approach’’ (using proxies) that could be applied to retail clients and facilitate the EUT alignment exercise. Also, several measures are already proposed by FIs or regulators to orientate households’ choices toward more energy efficient solutions (e.g., green mortgages with lower interest rates to support demand, energy efficiency advisory services). Considering the low level of alignment, those actions still need to get a better outreach to achieve the EU Fit for 55 objectives10.

It is worth noting that overcoming these usability challenges will be beneficial in the GAR context but also enhance FIs' capacity to access the European Green Bond market. Indeed, the voluntary European Green Bond Standard (EU GBS) will require issuers to allocate most of proceeds to assets aligned with the EUT. Facilitating FIs access to the European Green Bond market can also support the success of this (for now) voluntary scheme as financial corporates represent a material share of labelled bonds issuers.

After this crash test, the GAR is likely to stay under the spotlight and may see its credibility diminished (at least, considering its current version). Nevertheless, having extensively elucidated its limitations and subjected it to real-world testing, stakeholders (e.g., FIs, regulators) are now conscious of the challenges encountered and should actively work to address those. This will be crucial not only for reporting purposes but also for ensuring the success of the EU sustainable finance framework.

Armand SATCHIAN

ESG Analyst

La Française Asset Management

1The eligibility version represents the percentage of assets eligible to the EU taxonomy (eligible assets/total GAR assets). Taxonomy eligibility indicates if an economic activity is in the scope of the Taxonomy.

2European Commission, COMMISSION DELEGATED REGULATION (EU) 2021/2178 of 6 July 2021, 10 December 2021, Publications Office (europa.eu).

3EBA, EBA publishes results of EU-wide pilot exercise on climate risk, 21 May 2021, EBA publishes results of EU-wide pilot exercise on climate risk | European Banking Authority (europa.eu).

4There are two versions of the GAR KPI - a turnover version and a CAPEX version. While the turnover version considers the proportion of Taxonomy-aligned revenues of the respective counterpart, the CAPEX one is based on the proportion % of the proportion of Taxonomy-aligned CAPEX of the respective counterpart.

5EBF, Green Asset Ratio cannot be to sustainability what CET is to capital, January 2024, Green-Asset-Ratio-January-2024-002-2.pdf (ebf.eu)

6Assets consistently removed from the GAR calculation (not even in the denominator) are sovereigns’ assets, central bank exposures, supranational issuers and the trading portfolio.

7EBA, Final draft implementing technical standards on prudential disclosures on ESG risks in accordance with Article 449a CRR, EBA draft ITS on Pillar 3 disclosures on ESG risks.pdf (europa.eu)

8Platform on Sustainable Finance, Final Report on Minimum Safeguards, October 2022, Final Report on Minimum Safeguards (europa.eu) P. 54 ‘’ Financial institutions carrying out this activity would have to meet MS in order to be able to count these activities as taxonomy-aligned This would not be required, for example, for mortgages where the underlying activity is considered eligible (i.e. activities 7.1, 7.2 and 7.7) and whose descriptions do not include the term ‘financing’.

9Climate Change Adaptation DNSH is the only relevant DNSH criteria for mortgages.

10 The Fit for 55 refers to the EU's target of reducing net greenhouse gas emissions by at least 55% by 2030.